Our tool for managing your permission to our use of cookies is temporarily offline. Therefore some functionality requiring your consent to use of cookies may be missing.

MINI FINANCIAL SERVICES CUSTOMER COMPLAINTS.

MINI Financial Services, a trading name of BMW Financial Services (GB) Limited, is committed to providing products and service of the highest standard. If for any reason you feel we have not lived up to your expectations or you are not entirely satisfied with any aspect of our service please let us know. The information shown below provides a brief overview of how we deal with complaints, our customer complaints process and where to direct any complaints.

MINI Financial Services will investigate all complaints competently, diligently and impartially obtaining additional information as necessary. Every complaint will be assessed fairly, consistently and promptly taking into account all relevant factors to ensure a fair outcome for the customer.

Quick Access to MINI Financial SERVICES complaints.

MOTOR FINANCE REDRESS SCHEME.

In January 2024, the Financial Conduct Authority (FCA) paused the usual time limits for handling some motor finance commission complaints. This was while it reviewed past commission arrangements across the motor finance industry.

Following its review, the FCA published its final rules for a redress scheme on 30 March 2026. However, some parts of the scheme are being challenged. We don’t expect to know the outcome of this challenge until early 2027. Although we are not involved in the challenge, the FCA has agreed that parts of the scheme will be paused. Whilst there is a pause, we’re continuing to prepare for the scheme.

If you’ve already sent us a complaint, you don’t need to do anything else at this stage.

We’ll keep your complaint on hold for now. We’ll continue to monitor developments and contact you as soon as we can move your complaint forward. Your right to have your complaint considered will not be affected by these temporary arrangements.

The pause only applies to complaints that fall within the FCA’s redress scheme. If your complaint is outside the scheme, we’ll handle it under the FCA’s normal complaint-handling rules. We’ll contact you to explain what happens next.

If your agreement is within the scheme but no redress is due, we’ll also contact you in line with the latest FCA timelines.

You can find the latest information and timelines on the FCA website here.

FAQs – MOTOR FINANCE REDRESS SCHEME.

If you already have registered a complaint with us, no further action is required by you. We will provide further updates once we have completed our review and received guidance from the FCA. For the latest information regarding the FCA consultation, please click here.

You should check your contract with the CMC to see what it says about termination and your right to withdraw from the agreement. We will continue to correspond with the CMC until we receive confirmation from them that you have terminated your agreement. Once we receive this, we will update our records and contact you directly.

You can register a complaint here.

Please provide vehicle registration, finance agreement number and any other previous postcode / surname at the time of your agreement.

If you entered into a regulated motor finance agreement on or after 6 April 2007 where commission was paid, you’re likely to be eligible to make a complaint. This will include Select, Hire Purchase, Lease Purchase and Contract Hire agreements.

This applies for any type of commission, e.g. a discretionary or a non-discretionary one.

Typically, the amount of commission earned by a dealer or broker was determined by the interest rate that the agreement had been contracted at – the lower the interest rate, the lower the commission the dealer or broker received, and vice versa. This was known as a discretionary commission arrangement. Since January 2021, this commission model is no longer allowed.

This is usually referred to as a fixed commission. This means a fixed amount is paid by us and is calculated based on the vehicle you buy or as a percentage of the amount you borrow. The dealer or broker doesn’t have any discretion to vary the interest rate or APR you pay under your finance agreement.

Please complete our discretionary commission enquiry form by clicking the link below

You’ll need vehicle registration, finance agreement and any other previous postcode / surname at the time of your agreement.

- If we’ve sent you a confirmation of your commission model type, we’ll automatically log a commission complaint on your behalf and send you a letter of acknowledgement.

- No further action is required from you. We’ll investigate your complaint but won’t be able to send a final response until after the FCA commission complaints pause, i.e. after 31 May 2026.

A commission enquiry can take us a while to respond to if we can’t match your information to our records but we will come back to you and ask for additional information.

We’ll acknowledge receipt of your complaint within 8 weeks. After the FCA has issued its new rules, we’ll start to respond to complaints after 31 May 2026.

For the latest information from the FCA, please click here.

MINI FINANCIAL SERVICES COMPLAINTS PROCEDURE

How to complain about your finance agreement.

For a new complaint, please complete the complaint form by clicking on the button below.

Contact us.

We’re here:

9am – 5.00pm Monday to Friday

Email us at: csescalations@bmwfin.com

Write to us at:

Customer Escalations Team

MINI Financial Services

Summit ONE

Summit Avenue

Farnborough

Hampshire

GU14 0FB

Call us on: 0370 5050 197

Calls are charged at the local rate, plus your phone company’s access charge.

To help us investigate and try to resolve your complaint, please provide us with the following information:

- your name and address;

- your agreement number, if you have one;

- details of how we can contact you;

- a clear description of your complaint;

- details of what you would like us to do to rectify the situation;

- and if appropriate, copies of any relevant supporting documentation

We will do our best to resolve your complaint quickly, and will send you a Summary Resolution Letter if your complaint is resolved by close of the third business day following receipt of your complaint; or:

- within 5 working days, provide a written acknowledgement of your complaint and give you the details of who is handling the case and how to contact them,

- keep you updated on the progress of your complaint, and

- within 8 weeks of receiving your complaint, we will either:

- write to you with our final response and the reasons for providing this response, or

- explain why we are not in a position to give you a final response and let you know when we expect to be able to provide it, and

- in each case provide you with the contact details for the Financial Ombudsman Service

If you are dissatisfied with either our final response, or the reasons for any delay in providing our final response within eight weeks from the day we received your complaint, you can usually ask the Financial Ombudsman Service for an independent review.To be able to ask them for an independent review you must have given us the opportunity to find a resolution first and you must be: a private individual, or a business, charity or trust with an annual turnover of less than 2 million euros and fewer than 10 employees. If you wish to pursue your complaint to the Financial Ombudsman Service you must do so within 6 months from the date on which we send you our final response letter.

Call us on: 0300 123 9 123

Calls are charged at the local rate, plus your phone company’s access charge.

We're here:

8am - 8pm Monday to Friday (excluding bank holidays)

9am - 1pm Saturday

Email us at: complaint.info@financial-ombudsman.org.uk

Write to us at:

The Financial Ombudsman Service

Exchange Tower

London

E14 9SR

We are also members of the British Vehicle Rental and Leasing Association (BVRLA). All vehicles returned to MINI Financial Services are inspected in line with the British Vehicle Renting and Leasing Association fair wear and tear guidelines. This ensures that all customers are treated fairly with regard to any potential charges upon the vehicle return.

Unresolved complaints may also be referred to them by visiting their website www.bvrla.co.uk.

Or by email to: complaint@bvrla.co.uk

Or by writing to them at:

BVRLA

River Lodge

Badminton Court

Amersham

HP7 0DDor by Fax: 01494 434499

MINI INSURANCE SOLUTIONS.

For details of how to make a complaint in relation to your MINI Insurance, please select the appropriate insurance product and policy document on the MINI Insurance Solutions page.

The FCA’s deadline (29th August 2019) regarding Payment Protection Insurance Complaints (PPI) has now passed. MINI FS will therefore not consider any complaints about PPI we receive after this date.

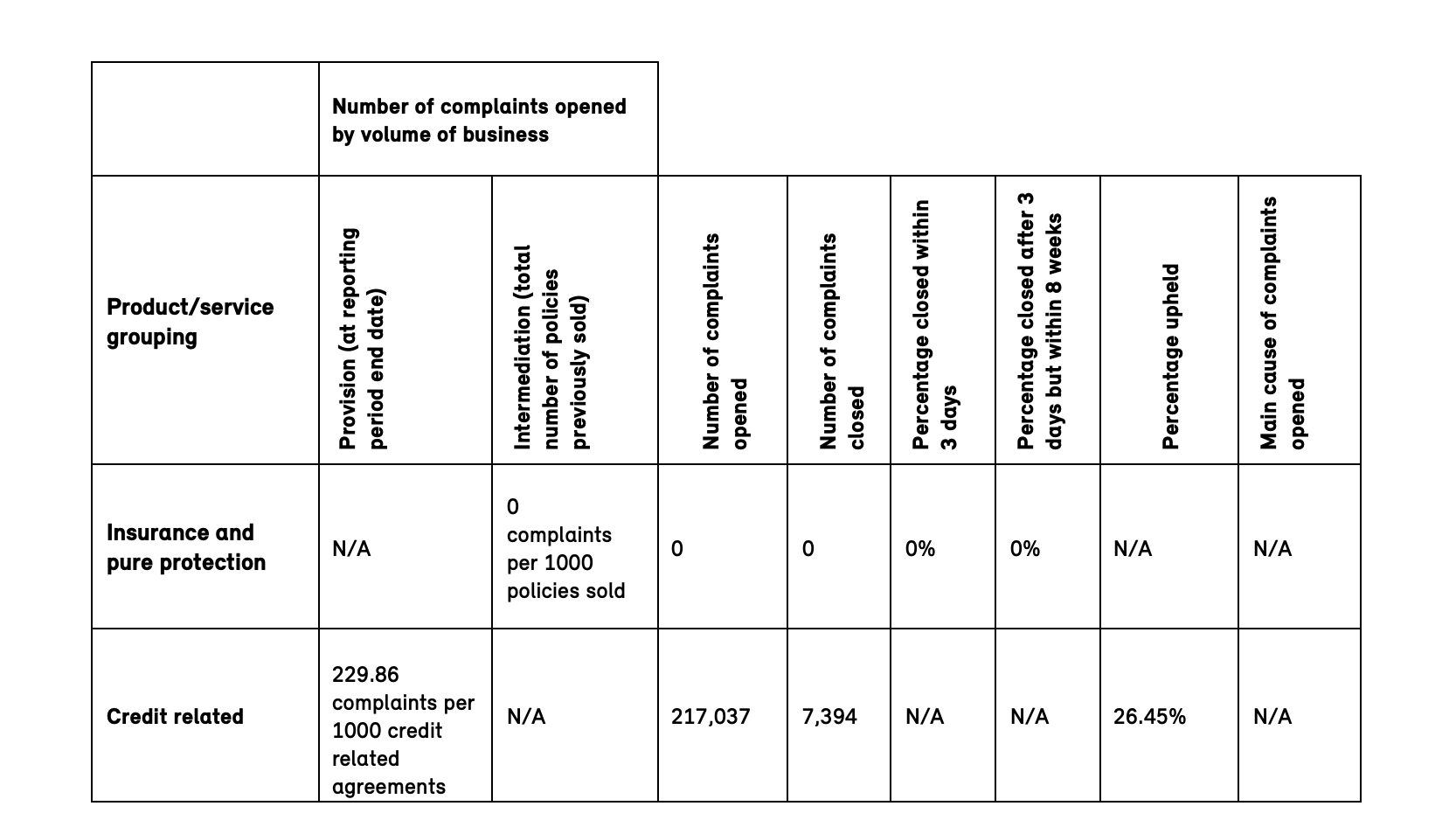

COMPLAINTS DATA.

COMPLAINTS PUBLICATION REPORT.

Firm name: BMW Financial Services (GB) Limited

Other firms included in this report (if any): None

Period covered in this report: 1st July 2025 – 31st December 2025

Brands/trading names covered: BMW Financial Services, MINI Financial Services, BMW Motorrad Financial Services, ALPHERA Financial Services, Rolls-Royce Motor Cars Financial Services, BMW Contract Hire, BMW Group Financial Services, ALPHERA Insurance Solutions, BMW Finance, BMW Group Insurance Solutions, BMW Insurance Solutions, BMW Motorrad Finance, BMW Motorrad Insurance Solutions, MINI Finance, MINI Insurance Solutions.

To help you put these figures into context:

The number of insurance related complaints opened during the reporting period is equivalent in volume to 0 complaints per 1000 Insurance and pure protection policies previously sold.

BMW Financial Services (GB) Limited along with other motor finance firms has received a significant increase in complaints linked to Discretionary Commission Arrangements (“DCA”). The FCA has paused the usual 8-week deadline for issuing Final Responses for these types of complaints, therefore the figures above show a high number of unresolved complaints. Further, the ratio of complaints opened per 1,000 credit-related regulated agreements is also higher, as a result of the significant increase in complaints linked to DCA.

The number of credit related complaints opened during the reporting period is equivalent in volume to 229.86 complaints per 1000 credit-related regulated agreements in place on 31st December 2025.